Under the Spotlight: Meta Platforms ($META)

.png%3Fbranch%3Dodyssey&w=3840&q=100)

Meta just delivered its fastest revenue growth in years – and its biggest spending bill ever. It was enough to send the share price plunging over 9%, but was the reaction warranted?

.jpg&w=3840&q=100)

ICYMI: Do your own research and make your own decisions. This article drills down on a specific company, however, it is not a recommendation to invest in the company and should not be taken as financial advice. Got a stock you want covered? Tell us here.

Meta Platforms ($META) just delivered one of its strongest quarters on record, in what Mark Zuckerberg called a ‘milestone quarter.’ The market didn’t buy it.

Revenue jumped 33% year on year to US$56.3B in Q1 beating expectations, operating margin held at a very healthy 41%, and the company still reaches more than 3.5B people across its apps daily – almost half the global population. On most earnings scorecards, that would be enough to earn a small round of applause.

Instead, Meta shares fell by over 9% after the result, with the market zeroing in on one line in particular: capital expenditure. Meta now expects to spend between US$125B to US$145B on capex this year, up from its previous forecast of US$115B to US$135B.

That’s the Zuckerberg trade off summed up: the business has never been better, the bill has never been bigger, and investors aren't sure which one matters more.

The ad machine

For all the talk of AI agents, superintelligence and smart glasses, Meta is still, first and foremost, an advertising business.

The company reports in two main segments. Family of Apps includes Facebook, Instagram, Messenger, WhatsApp and other services. Reality Labs includes its virtual and augmented reality hardware, software and content. One makes almost all the money, while the other rides projections.

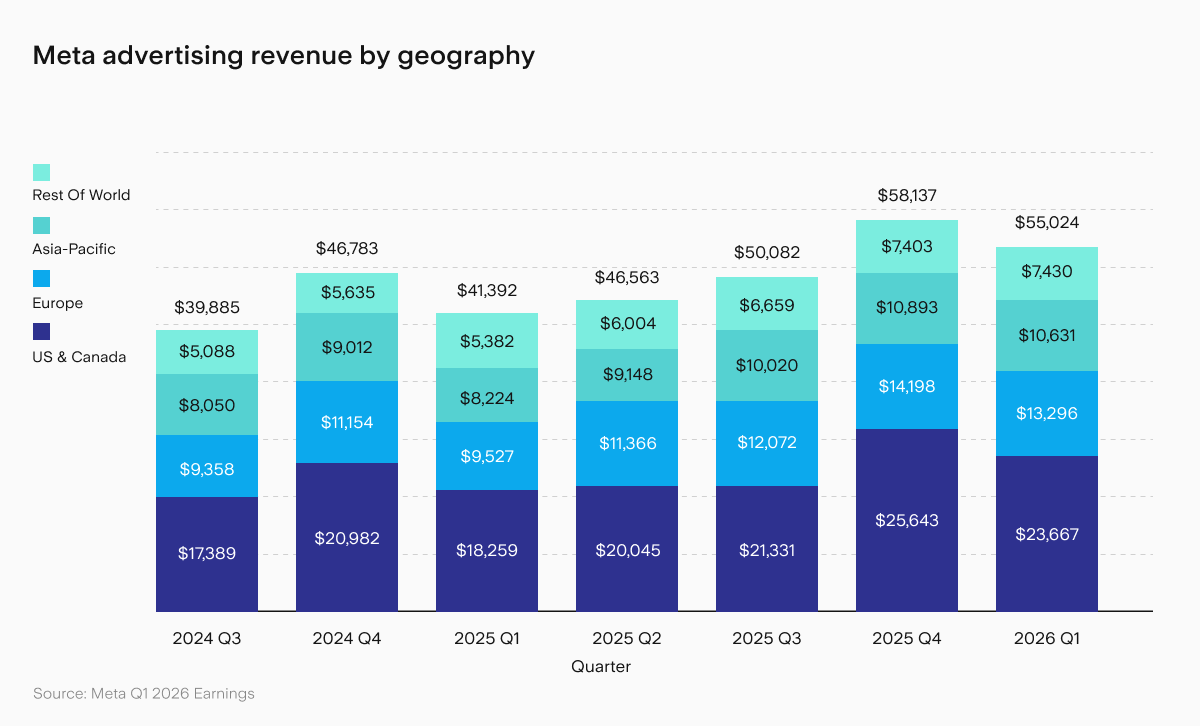

In Q1, Family of Apps generated US$55.9B in revenue, while advertising alone brought in US$55.0B. That means ads made up almost 98% of Meta’s total revenue.

This is where AI is really earning its keep. Not through Zuckerberg’s grand vision of AI agents helping billions of people manage their lives. At least, not yet. But in the slightly less glamorous business of showing better ads to more people at better prices.

Meta’s ad impressions rose 19% year on year, while the average price per ad increased 12%. That helps explain why average revenue per app user rose to US$15.66, up from US$12.36 a year ago. Meta is getting better at monetising each user.

Meta says its AI systems are improving recommendations across Facebook, Instagram and ads. In other words, Meta's algorithm is getting better at keeping you glued to your screen – time spent on Instagram Reels rose 10% in Q1, while Facebook video time climbed more than 8% globally.

.png&w=3840&q=100)

This isn't the sexiest part of the AI story. But for investors, it may be the most important one.

Zuck's AI era

The bigger story is where Meta wants to go next.

Meta has spent the past few years trying to convince investors that it’s not just the company your uncle uses to post holiday photos on Facebook. First came the metaverse pivot. Now its sights are on AI.

The latest push is Meta Superintelligence Labs, which released its first model, Muse Spark, during the quarter. Muse Spark now powers Meta AI across direct chat threads, the standalone app and website. Zuckerberg says Meta is building personal agents and business agents that can help people achieve goals, run tasks and support businesses.

Meta wants AI inside its apps, ads, business tools and glasses. The pitch is that AI will not just answer questions, it’ll understand what users want and act as a digital assistant across daily life.

There are signs of traction. Meta says sessions per user increased by double digits after the rollout of Muse Spark. Business AI conversations have grown from 1M a week at the start of the year to more than 10M. More than 8M advertisers are using at least one of Meta’s generative AI ad creative tools.

Then there are the glasses. Daily usage of Meta’s AI glasses has tripled year on year, helped by new Ray-Ban and Oakley products. For now, they remain a relatively small business. But for Zuckerberg, they are clearly part of the long game: AI that doesn’t just live in a chat box, but sits on your face. Very normal. Very Silicon Valley.

The Capex catch

The problem is that all these growth projects cost a lot of money.

Meta spent US$19.8B on capex in Q1 alone, up from around US$13.7B a year earlier. Its new full-year forecast of US$125B to US$145B is a major step-up and an admission that the AI buildout Meta needs for ROI is more expensive than anticipated.

To be fair, Meta is not alone. Amazon ($AMZN), Alphabet ($GOOGL) and Microsoft ($MSFT) are also spending huge sums on AI infrastructure. Alphabet has lifted its 2026 capex outlook to US$180B to US$190B, Amazon has pointed to around US$200B of AI-related investment, and Microsoft’s lifted its spend to US$190B.

But there is one key difference. Amazon, Microsoft and Google have cloud businesses where customers are directly paying for AI infrastructure. Meta’s return is less direct. It comes through better engagement, better ad targeting and the hope that future AI agents become products people and businesses actually use.

That may still be a great return. Meta has one of the largest distribution networks on earth and a core ad business that’s already benefiting from AI. But it’s harder to model than cloud revenue subscriptions, and markets are sceptical about the future payoffs.

Valuation check

Following the post-result fall, the stock is on a P/E of 22.97. That’s not bargain-bin cheap, but it also does not look outrageous for a company growing revenue at 33% with a 41% operating margin.

The analyst view remains firmly positive. On Stake Black, all but one of the 19 analysts covering the stock currently give Meta a ‘buy rating, with an average price target of US$831, around 36% above the current share price.

The caveat is that Meta’s headline earnings were flattered by an US$8.03B tax benefit. Reported EPS was US$10.44, but without that benefit, EPS would have been US$7.31. Still strong, just not quite as heroic as the headline number first suggests.

Is it a buy?

The bull case is straightforward. Meta’s ad engine remains one of the best businesses in global tech. AI is already improving engagement, ad performance and advertiser tools. The company has huge scale, strong margins and enough cash flow to fund its ambitions.

The bear case is also easy to see. Meta is spending enormous amounts on an AI future that is still difficult to value. Reality Labs continues to lose billions. Regulatory risks remain a drag. And the latest user numbers showed a slight quarter-on-quarter dip in daily active people, even if Meta blamed disruptions in Iran and Russia.

For investors, Meta is not really a question of whether the business works. It does. The question is whether the AI spending will strengthen the ad machine or slowly turn into another expensive Zuckerberg side quest.

For now, the market is saying: impressive quarter, scary bill.

This is not financial advice nor a recommendation to invest in the securities listed. The information presented is intended to be of a factual nature only. Past performance is not a reliable indicator of future performance. The author of this article and other employees of Stakeshop Pty Ltd may hold positions or have financial interests in the company (or companies) discussed above. As always, do your own research and consider seeking financial, legal and taxation advice before investing.

Senior Markets Commentator

Kylie Purcell is an investments analyst and finance journalist with over a decade of experience covering global markets, investment products and digital assets. Her commentary has been featured in publications including the Australian Financial Review, Yahoo Finance and The Motley Fool. She has a Masters Degree in International Journalism from Cardiff University and a Certificate of Securities and Managed Investments (RG146).

Subscribe

By subscribing, you agree to our Privacy Policy.

.png%3Fbranch%3Dodyssey&w=3840&q=100)

.png%3Fbranch%3Dodyssey&w=3840&q=100)

.png%3Fbranch%3Dodyssey&w=3840&q=100)